On a dusty highway in northern Nigeria, a businessman once decided to delay expansion – not because of lack of demand, but because of a lack of financing commensurate with his values. That difference is bigger than a business. Today, more than 40% of Nigerian adults are economically disadvantaged, while the country faces a $21 trillion housing deficit and long-term infrastructure gaps. Yet, within this obstacle lies opportunity.

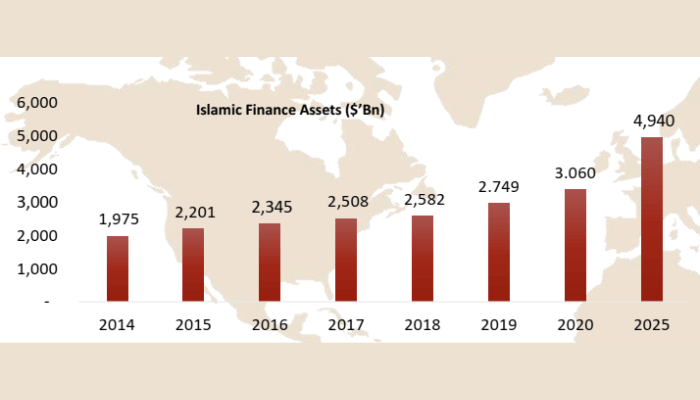

Globally, Islamic finance assets are projected to exceed $4.94 trillion by 2025, growing at about 8% annually, while Nigeria's market, with heavy concentration in banking parallel to conventional financing, is only $2.3 billion – barely 0.52% of GDP, according to the Islamic Finance Development Indicators (IFDI) report.

Sukuk, which is already used by the federal government to raise over ₦612 billion for roads, provides a bridge between capital and real assets. Institutions like TajBank are now stepping into this gap – redefining trust, inclusion and access in a system where finance is not just about returns, but about alignment.

If there is trillions of naira of unmet demand, millions of disenfranchised Nigerians, and a booming global Islamic finance market already in place, the real question is no longer whether non-interest finance can work in Nigeria – but whether the ecosystem can grow fast enough to meet the moment.

The rise of non-interest finance: from niche to strategic asset class

Once a marginal segment, non-interest finance is rapidly repositioning itself within Nigeria's financial architecture, driven by macroeconomic pressures and the growing preferences of investors. Persistent inflation, currency volatility and rising borrowing costs have exposed the limitations of traditional lending models, prompting both issuers and investors to seek alternatives that are more flexible and asset-backed. The Nigerian non-interest finance market was valued at $2.30 billion at the end of 2021, ranking 13th on the Islamic Finance Development Indicator. Nigeria's non-interest finance market lags far behind its peers, representing only 0.075% of the global Islamic finance market, which was valued at $3.06 trillion at the end of 2021.

For over a decade, the non-interest finance industry in Nigeria has grown strongly supported by good demand, increased awareness, capacity building and regulatory support.

In this context, Sukuk have emerged as a reliable instrument – linking financing directly to tangible assets and embedding risk-sharing mechanisms that align returns with real economic activity.

Globally, Islamic finance assets are projected to exceed $4.9 trillion by 2026, yet Nigeria's market remains significantly underpenetrated, suggesting substantial room for growth. Domestically, sovereign sukuk issuances have demonstrated both depth of demand and practical impact, particularly in infrastructure financing, where funds are linked to identifiable projects such as roads and housing. This asset-backed structure increases transparency, strengthens investor confidence, and mitigates some of the risks associated with pure debt financing.

As awareness deepens and the regulatory framework matures, non-interest finance is transforming from a trust-based space to a strategic asset class – one that offers a path to diversification, sustainability and long-term capital raising in Nigeria’s evolving financial landscape.

Sukuk as Infrastructure Capital: Bridging Nigeria's Financing Gap

Nigeria's infrastructure deficit – running into trillions of naira – is hampering economic productivity, from congested highways to a housing shortage estimated at more than 28 million units. Traditional funding sources, which largely rely on budgetary allocations and conventional borrowing, have proven inadequate to bridge this gap. In this context, Sukuk are emerging as a viable and increasingly strategic financing instrument, linking capital market resources directly to real sector assets.

Unlike traditional bonds, Sukuk structures are asset-backed, ensuring that funds raised are linked to identifiable projects such as roads, housing and energy infrastructure. This model not only increases transparency and accountability but also aligns investor returns with the performance of the underlying assets. Nigeria’s sovereign sukuk program has already demonstrated this potential, raising over ₦612 billion since 2017 to finance critical road infrastructure across the country.

Beyond government issuance, the opportunity lies in raising corporate and subnational sukuk to unlock private capital for infrastructure and housing. As fiscal pressures increase, Sukuk provide a route to raise long-term, ethical and diversified financing to bridge Nigeria's financing gap while deepening Nigeria's capital markets.

TajBank's strategic play: growing Islamic finance in the conventional market

Operating within a financial system where non-interest banking accounts for barely 1% of total banking assets, TajBank is positioning itself as a catalyst for scale in Nigeria's underpenetrated Islamic finance market. With the industry valued at approximately $2.3 billion – only 0.52% of GDP, the potential for growth remains significant, especially against global market projections.

TajBank's strategy focuses on three levers. Firstly, product innovation, including sukuk structuring and participation in ethical financing models that align capital with real sector assets. Second, through retail penetration, accessible, value-aligned financial products targeting the financially excluded population – over 40% of Nigerian adults. Third, institutional participation, unlocking liquidity from pension funds, asset managers and corporate issuers, which are increasingly allocating to non-interest bearing instruments.

By combining trust-based banking with scalable financial structures, TajBank is not just participating in the market – it is helping to expand it, establishing non-interest finance as a viable option within Nigeria’s evolving capital ecosystem.

Investor behavior and confidence: the missing link in sukuk adoption

Despite strong structural advantages, Sukuk adoption in Nigeria remains a barrier less to product design than to investor behaviour. Awareness is still limited: non-interest finance contributes about $2.3 billion, only 0.52% of GDP, while sukuk constitute a minor share of the domestic capital market. For many retail investors, perceived complexity, limited product familiarity and low financial literacy create friction, even where instruments are asset-backed and ethically aligned.

Behavioral biases also play a role. Investors often default to familiar traditional products, demonstrating status quo bias and risk aversion, especially in volatile macroeconomic conditions. For institutional investors, barriers around liquidity, secondary market depth and benchmark comparability further reduce participation.

Bridging this gap requires more than product availability – it requires trust architecture. Clear communication, demonstrable project results, simplified product structures and continuous investor education are essential. Without overcoming behavioral barriers, sukuk risk remaining an unattractive concept with limited market penetration.

Policy, regulation and market depth: the next growth frontier

The expansion of Nigeria's Islamic finance ecosystem will depend less on product innovation and more on policy coherence and market architecture. While progress has been made through regulatory guidelines and sovereign sukuk issuance – now worth over ₦612 billion – the market remains shallow with limited corporate participation and low secondary trading. To transform Sukuk from episodic issuance to a mainstream financing instrument, three policy priorities are important.

Due to the asset-backed nature of non-interest finance transactions, this sector has a good performance in the real estate sector. It can be used to solve some challenges in mortgage entry; and consumers' disinterest in commercial financing opportunities due to trust-based concerns over interest.

First, regulatory clarity and coherence across all agencies—CBN, SEC, FIRS—should reduce structuring uncertainties and approval timelines. Second, tax neutrality is necessary to eliminate the double taxation risks inherent in asset-backed structures, ensuring that sukuk can compete fairly with traditional bonds. Third, secondary market development – through liquidity frameworks, market-making incentives and institutional participation – will enhance price discovery and investor confidence.

Ultimately, the next phase of development will be defined by coordination. Without this, sukuk remain promising; With this, Nigeria can unlock a scalable, inclusive and flexible financing ecosystem